Key Takeaways

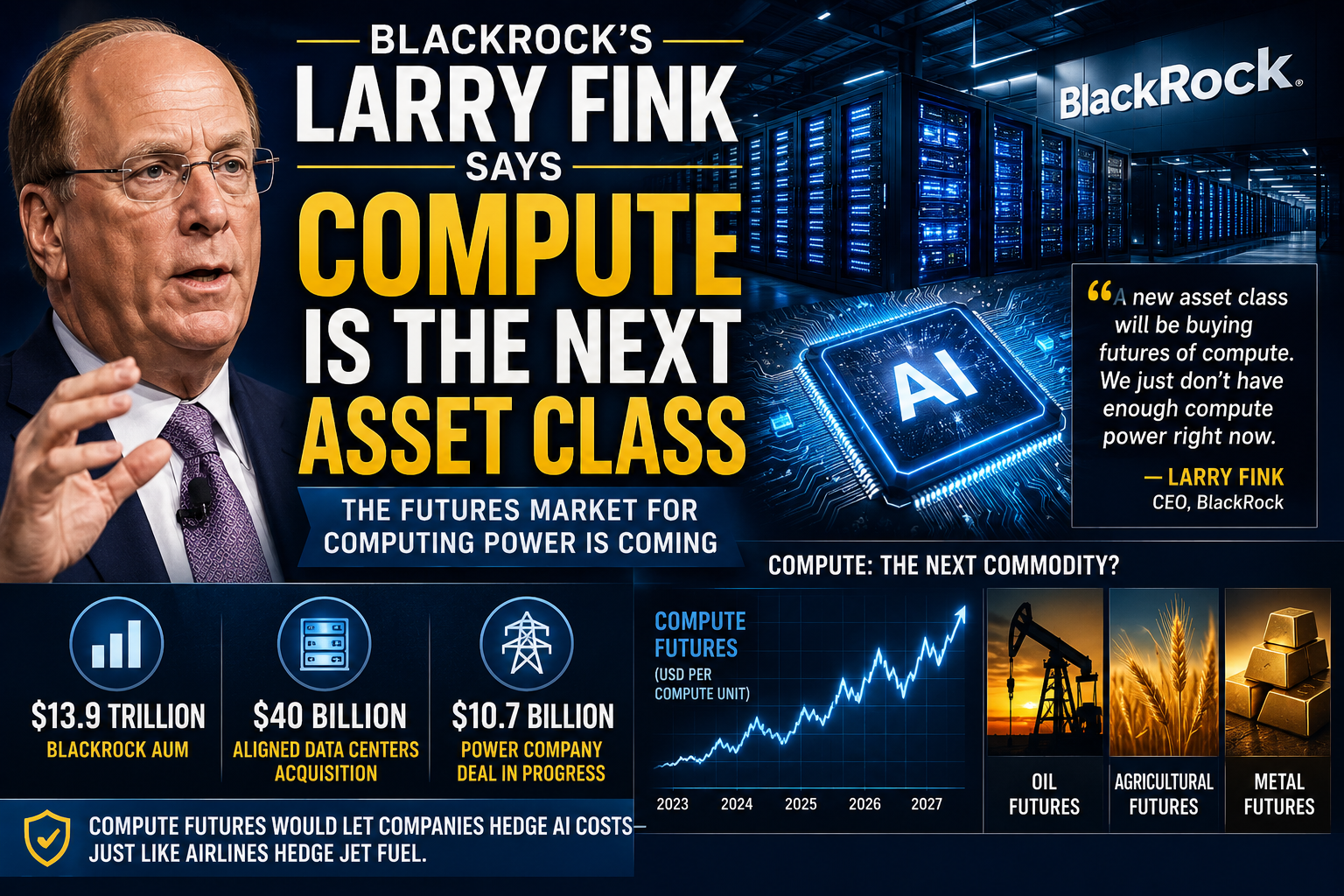

- BlackRock CEO Larry Fink told the Milken Institute that computing power will become a tradable futures market — similar to oil and agricultural commodities.

- Fink warned the US is short compute, chips, memory, and power — calling it a supply crisis, not a bubble.

- BlackRock is backing this view with capital: a $40 billion data center acquisition, a $10.7 billion power company deal, and partnerships with Microsoft, Nvidia, and MGX.

- For institutional investors, compute futures would allow hedging AI infrastructure costs the same way airlines hedge jet fuel.

| Stat | Value |

|---|---|

| BlackRock AUM | $13.9 trillion |

| Aligned Data Centers acquisition | $40 billion |

| Tokenized finance sector size | $30 billion (tripled in one year) |

The Prediction

Speaking at the Milken Institute Global Conference in Beverly Hills on May 5, BlackRock CEO Larry Fink made a prediction that received less attention than it deserved. Compute, he said, will become a new asset class. Not a metaphor — a literal futures market where institutional investors buy and sell contracts on raw computing power, the same way they hedge crude oil or agricultural commodities today.

"A new asset class will be buying futures of compute. We just don't have enough compute power right now." — Larry Fink, CEO BlackRock

Fink's framing was deliberate. He placed compute alongside energy and food — essential inputs to the modern economy that are both scarce and price-volatile. When commodities reach that threshold, financial markets price them through derivatives. Fink is saying compute has crossed that threshold.

The Supply Crisis Behind the Prediction

The prediction is grounded in a specific diagnosis. Fink identified four simultaneous shortages holding back AI expansion: compute capacity, semiconductor chips, memory, and electrical power. These are not independent problems — they compound each other. A data center cannot run without power. A chip cannot function without memory. The entire stack is constrained simultaneously, and investment capital alone cannot solve a physical infrastructure problem overnight.

BlackRock is not just predicting this market — it is building the underlying infrastructure that would make such a market possible. Its Global Infrastructure Partners division agreed to acquire Aligned Data Centers for approximately $40 billion. A separate consortium involving BlackRock and EQT is pursuing AES Corporation, a major power provider, for $10.7 billion. These are not passive index fund positions. They are direct ownership stakes in the physical layer of AI infrastructure.

What Compute Futures Would Mean for Investors

The practical implication for institutional portfolios is significant. Today, a company building AI products has no way to hedge its compute costs. It pays whatever the cloud provider charges — Amazon, Microsoft, or Google — with no forward price certainty. A compute futures market would change that. Technology companies could lock in pricing for future compute capacity the same way airlines lock in jet fuel prices through forward contracts, reducing earnings volatility and enabling more predictable capital planning.

For asset managers, compute futures would create a new source of uncorrelated return. Infrastructure investments tied to data centers and power generation already offer inflation protection and long-duration cash flows. A derivatives layer on top of that infrastructure would add liquidity and price discovery that the asset class currently lacks.

The Standardization Problem

The one genuine obstacle Fink acknowledged is definitional. Futures markets require standardized contracts — a benchmark unit that all parties agree measures the same thing. For oil that is a barrel. For wheat it is a bushel. For compute, the industry has not yet settled on an equivalent. Performance per watt, latency guarantees, and availability windows all vary across hardware generations and AI workload types. Until a standard unit emerges, exchanges cannot list contracts.

BlackRock's positioning suggests the firm believes that standard is arriving sooner than markets currently price. Its move into direct infrastructure ownership — rather than simply financing data center developers — indicates it expects to help set that standard rather than wait for someone else to define it.

The Investor Takeaway

Fink's Milken prediction is best understood not as a forecast of a distant future but as a signal about where the world's largest asset manager is deploying capital today. BlackRock's $40 billion data center acquisition and its $10.7 billion power company pursuit are the physical manifestation of a conviction that compute is becoming a commodity. When the futures market eventually emerges — and Fink is betting it will — BlackRock intends to already own the underlying asset.

For institutional investors watching from the sidelines, the question is not whether compute futures will exist. It is whether your portfolio has any exposure to the infrastructure that will underpin them.

Zulfiqar Ali Mir holds a PhD in Econometrics and an MFE degree. He is the founder of Black Iron Times, a financial intelligence platform covering US markets, Federal Reserve policy, and institutional investment trends.